Crude Oil, Chemicals, Metals & Mining Theme, Electric Power, Energy Transition, Polymers, Ferrous, Renewables

March 25, 2025

Commodity Tracker: 5 charts to watch this week

Featuring S&P Global Commodity Insights

Eyes are on OPEC+'s output levels following the release of detailed plans to compensate for the bloc's overproduction. China's manufacturing index is improving, supporting steel margins, but uncertainties over the rest of the year cloud expectations of further growth. S&P Global Commodity Insights editors also watch supply-demand factors affecting petrochemicals prices, particularly Europe's polycarbonate and Brazil's recycled polyethylene terephthalate.

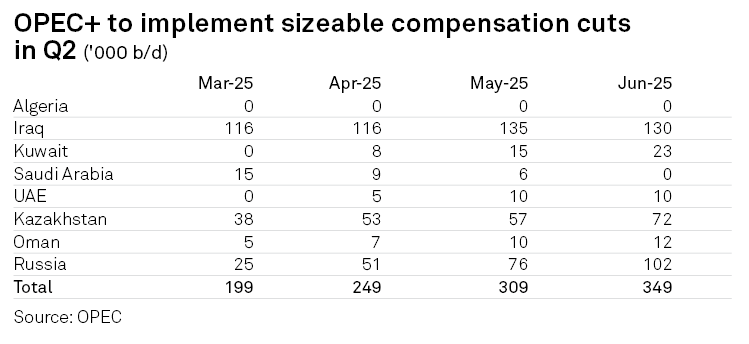

1. OPEC+ compensation cuts could outweigh higher output quotas

What's next? Intense scrutiny of the group's production levels will continue. If it sticks to its plans, the voluntary producers will cut between 199,000 b/d and 349,000 b/d monthly from March through June. OPEC+ can amend its strategy at any point if it sees market conditions requiring a change in approach. The next meeting of the Joint Ministerial Monitoring Committee that oversees the OPEC+ crude production agreement is scheduled for April 5. A full OPEC+ ministerial meeting is slated for May 28.

Related content: OPEC+ steers through uncertainty

2. China's manufacturing growth improves steel margins

What's happening? China's manufacturing production index of steel consumption produced by Platts stood at 115 for January and February, up 12 points from the same period in 2024. This is the highest year-on-year growth rate for January-February since 2021. The production index is based on production data from China's National Bureau of Statistics for 18 steel-intensive manufactured goods, categorized into seven sectors and weighted according to their share of steel consumption. The monthly production average in 2018 is used as the baseline of 100. The robust manufacturing activity so far in 2025 helped to support healthy steel margins amid rising steel production.

What's next? Market outlook for the manufacturing sector and its related steel demand remains uncertain for May and beyond, particularly in the second half of 2025, as the domestic consumer goods consumption, despite fiscal stimulus, is unlikely to improve much further given still weak household income expectations. Rising global trade barriers could also begin to adversely affect China's exports. The market consensus for now is that, in the best scenario, the growth in manufacturing steel demand is still insufficient to offset the decline in the property sector in 2025.

3. Polycarbonate price downtrend reflects challenging outlook for European producers

What's happening? Persistent weak demand has dragged down extrusion and general-purpose molding grade polycarbonate prices since peaking in July 2024. On March 19, Platts-assessed DDP NWE GP molding grade polycarbonate fell to Eur2,040/mt, the lowest price since the assessment began on March 1, 2024. An underperforming automotive sector and delayed demand restart from construction in Europe further exacerbate an already challenging landscape for European producers, where Chinese material has been competitive.

What's next? China is expected to remain a net importer of polycarbonate in 2025. However, Commodity Insights analysts expect this to flip by 2036 based on current estimates. China's push for self-sufficiency has resulted in additional investment in capacity expansion, further pressuring prices. There are still pockets of growth areas for polycarbonate, such as specialty films and more niche applications, including compounding and value-added markets.

4. Brazilian recycled PET market faces supply-demand imbalance

What's happening? Brazil's recycled polyethylene terephthalate market is seeing high prices due to limited feedstock supply. The price of post-consumer PET clear bottle bales (95/5) remains elevated despite recently falling from record highs above Real 6/kg on a DDP Sao Paulo basis. Platts, part of S&P Global Commodity Insights, assessed post-consumer PET clear bottle bales at Real 5.55/kg and R-PET clear flakes at Real 9.75/kg on March 21. The price gap between recycled and virgin resin is widening, deterring buyers from recycled materials. While sustainability awareness is growing, the appeal of R-PET is diminishing due to competitive virgin resin prices.

What's next? Market participants have mixed outlooks. Some are optimistic about continued support from companies with sustainability goals despite the cost disparity between recycled and virgin resin. Others are skeptical, noting a shift toward virgin resin use. Coca-Cola has delayed recycling targets, while Ambev has reduced the transparency of its disclosure, raising doubts about corporate sustainability commitments.

5. Increased snowpack raises hydro forecast, pulls down forwards

What's happening? Snowpack levels have increased in the Upper Colorado River Basin, boosting the hydroelectric outlook and pulling down power forward prices. Snowpack conditions above Lake Powell, located on the Utah-Arizona border, are at 95% of median, up eight percentage points since the beginning of March. In forwards, Palo Verde on-peak June is currently in the low $40s/MWh, down over $3.25 from early March. However, the water supply forecast at Lake Powell is at 70% of average for the April-July forecast period, up 1 percentage point from the early March. Lake Powell summarizes the hydrologic conditions throughout the Upper Colorado River Basin.

What's next? This week will continue to bring cold temperatures and waves of precipitation across much of the Great Basin and Upper Colorado River Basin. However, beyond the week, there is an increased chance for warmer and drier-than-normal conditions across much of the CBRFC area.

Reporting and analysis from Rosemary Griffin, Jing Zhang, Nate Zhang, Gustavo Kruger and Kassia Micek

Editor:

Barbara Caluag